Market moves continue to be intense, with heightened volatility in technology, precious metals, cryptocurrencies, and energy, amid ongoing talks between the US and Iran. On the macro front, last week’s data on job openings continued to suggest the US labour market remains soft, supporting Fed rate cuts in 2026, while in the Euro area, inflation has continued to improve (1.7% year-over-year in January). However, for the ECB, this is not yet enough to alter its “in a good place” stance. In the coming days, watch retail sales, inflation data and job creation for January in the US.

In these volatile markets, two themes are clearly emerging:

- Theme #1: “Diversification” of global portfolios remains a driving force, as evidenced by the outperformance of small caps, Emerging Markets and Europe vs. traditional market engines such as US large caps. Within the S&P 500, the equally weighted index is up 4.5% YTD relative to the classic index, and the Bloomberg Mag7 index is down by c. 4% YTD. This is in line with our expectations, as we have been tilting the equity bucket of our multi-asset portfolio towards Europe, US small caps and EM (ex-China) since mid-December 2025. Yet, the earnings season keeps signaling very robust earnings growth for the US Tech and Communication services sectors. In that context, it is worth keeping in mind that the demise of the US tech sector is an event which has been announced far more often than it has occurred.

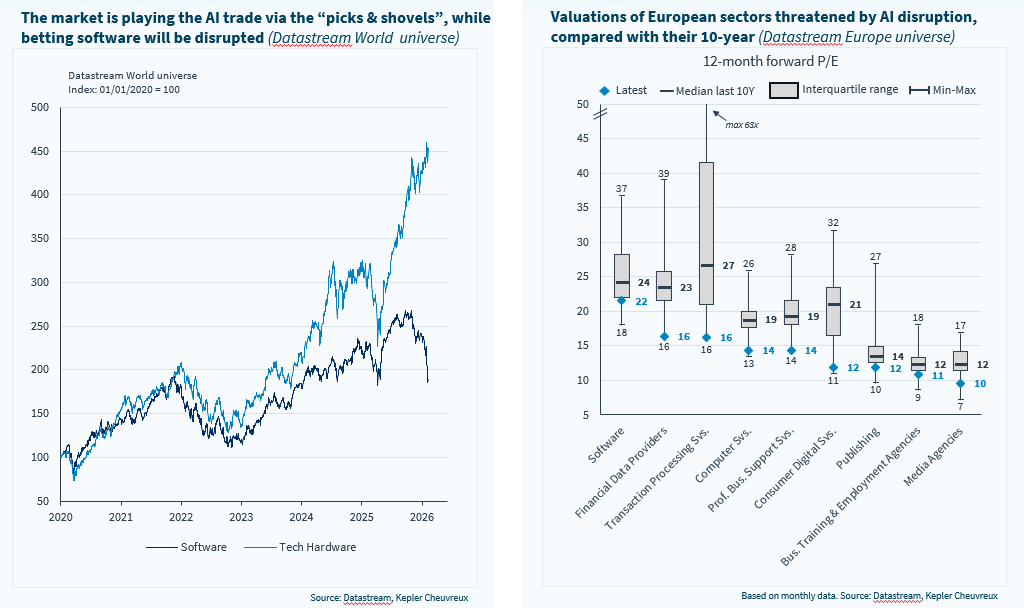

- Theme #2: “AI winners vs. AI losers” is the other clear theme emerging from sector performance. On an equally weighted basis across S&P sectors, there is a c. 30% gap between the standout performer this year, Oil & Gas, and the worst performer, Software. Media and Financial Services are also perceived as AI losers and are down significantly. The Oil & Gas sector has benefited from the ongoing Iran crisis, which triggered fears of supply disruptions, but it is also a large and cheap US sector with limited direct exposure to AI. In contrast, the next two top performers, Materials and Tech Hardware, are clearly among the “AI winners”, enjoying the booming data-centre buildout. However, there is one interesting – maybe less consensual – dynamic to note: consumer retail, consumer staples, and some parts of consumer discretionary are faring much better than the overall market.

In today’s weekly, we wanted to illustrate the above dynamics using a selection of charts to help navigate current markets.

Our views on the above topics are as follows:

- We keep playing the diversification theme for now. In that regard, Japan’s snap election and strong LDP majority reinforce the case for Japanese equities. We also keep an OW stance on Emerging Markets ex-China. We also left unchanged our exposure to gold, despite recent turbulences. Within the USD equity market, we reiterate our OW stance on small caps.

- We are not interested in buying falling knives among the AI losers (even where our equity analysts are constructive in many cases with strong fundamental arguments), as we fear it might take some time for companies to fully clear the associated risks. We keep preferring semis vs software within Tech, and our OW stance on utilities, which are now part of the AI ecosystem, remains a strong conviction.

- We find value in consumer sectors, arguing that Trump is likely to seek to win over consumers ahead of the midterms. Trump’s Big Beautiful Bill already includes a number of measures to stimulate mass consumption, but we are also hopeful about two potential levers: energy (we assume tensions with Iran will soften and Trump will avoid causing major disruptions that would cause a spike in oil prices) and interest rates (key to reviving auto and housing demand). We also believe it makes sense to revisit these sectors, as: 1) investors have been underinvested; 2) we note multiple bottom-up initiatives to revive top-line growth and slash costs; and 3) the process of disinflation continues.

- Should consumer sectors perform better, we believe several upstream sectors within the consumer value chain could benefit, notably packaging and chemicals. Chemicals have been a significant underperformer (both in the EU and US). In Europe, energy costs have compounded European chemical players’ problems, alongside a surge in Chinese capacities (and booming imports in Europe). As Europe continues to address its competitiveness, the German press (Handelsblatt) reported last week a potential sweetening of the European CO2 framework for heavy industries such as Chemicals (for a refresher on how the EU ETS system works, read our Head of Utilities’ comment here).

- More specifically, press reports suggest that the EU Commission may propose extending free allowances beyond the currently planned phase-out timeline. This might lead to lower CO2 allowance prices, likely putting a little pressure on wholesale power prices and reducing the cost of CO2 rights for European chemical companies. That said, our analysts note (here) that such a decision would, in fact, relieve future expenses rather than reduce current ones. In Chemicals, our analysts favour Bayer and BASF.

AI disruption fears weigh on software and data-related sectors