Recent days have been marked by renewed geopolitical tension with Iran and a fresh wave of trade uncertainty following the US Supreme Court’s decision on Trump’s tariffs. This adds to the ongoing “AI scare trade,” which continues to weigh on software, media and professional‑services equities. Autos and pharmaceuticals have also been volatile in Europe, though for stock‑specific reasons (e.g., Stellantis, Novo Nordisk).

Tariffs: The situation remains highly fluid, as Trump is now exploring alternative legal channels to impose tariffs, each with its own complexities. Still, the ruling is a setback for him and a reminder that US checks and balances remain intact. It also raises the odds that the Supreme Court will block Trump’s attempt to dismiss Lisa Cook. This dynamic supports short‑term dollar stabilisation, although Trump’s potential responses keep posing downside risks for the USD.

- Inflation & bonds: in the near term, US goods inflation may ease slightly, which is supportive for bonds. We also believe Trump may use this setback to modestly soften tariffs, offering some relief to US consumers ahead of the midterms while maintaining a narrative of policy consistency.

EU Industrial Accelerator Act: this week, we turn to the upcoming EU Industrial Accelerator Act. A draft is already circulating, with final proposals expected in the coming weeks. European policymakers face a clear need to accelerate structural reforms to restore industrial competitiveness and prevent further strategic slippage.

- Policy complexity: While the overarching goal is clear, the proposed targets are difficult to reconcile, and the Act risks becoming another overly complex policy package. Simplicity still seems elusive.

- The stated objectives are the following: reduce dependencies and vulnerabilities; safeguard industrial output in strategic sectors (Automotive, Base Metals, Chemicals, and Green Technology, especially batteries); boost investment in green products; establish a clear framework for foreign investment in those sectors.

- In practice, the Commission intends to impose rules with regard to public procurement and fiscal incentives: wherever public support is involved, “made in the EU” and low‑carbon criteria would apply. In Autos, the impact could be significant, given that corporate fleets account for ~60% of demand.

Autos outlook: Whether these measures can meaningfully support the European auto industry will depend on the final definitions: what counts as “EU made”? Will Korean and Japanese batteries qualify? Or must all batteries be manufactured within the EU? Additional issues also need to be addressed, particularly electrification targets. Our analysts remain cautious:

- The plan offers little short-term relief, while Chinese market share keeps rising and weakening domestic demand increases the risk of dumping abroad.

- If EU requirements push BEV (Battery Electric Vehicle) prices too high, consumers may still prefer cheaper, unsubsidised imports.

- Europe continues to face a capability gap in batteries, while OEMs (Original Equipment Manufacturers) will only invest if regulation is stable, predictable, and allows adequate returns. Recent comments from Stellantis underline the industry’s concerns. The 2035 electrification targets increasingly look unrealistic.

Our Investment stance:

- We remain cautious on “falling knives” in software, media and professional services. Some valuations appear attractive on historical metrics, but the paradigm has shifted: AI is both disruptive and deflationary for these sectors. We keep preferring network industries such as utilities and telecommunications, as well as infrastructure-related sectors to leverage the German stimulus plan.

- On Iran, we believe the political cost of escalating tensions remains high ahead of the US midterms. A large-scale strike could push oil above $90–100/b, an outcome likely to be very unpopular. Moreover, the strategic objectives (further constraining Iran’s nuclear programme or pursuing regime change?) remain unclear and complex.

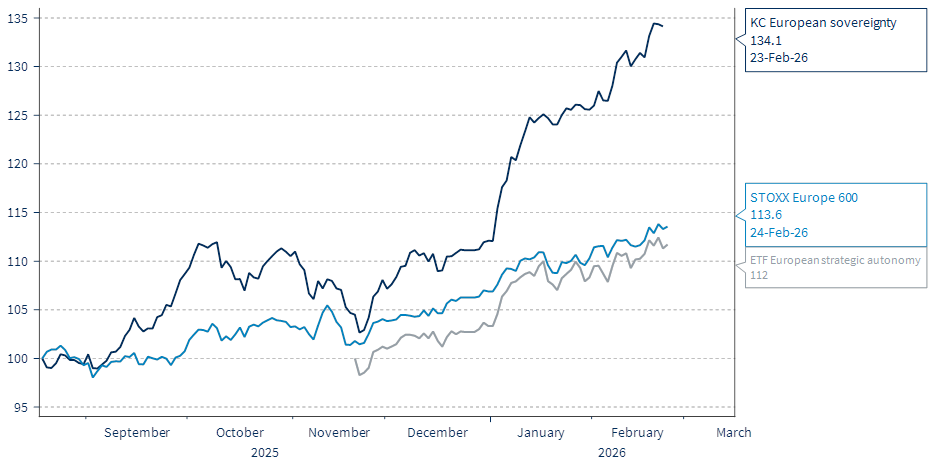

- As for EU competitiveness policies, we continue to favour our EU sovereignty strategy as the most effective way to capture the opportunity set while managing risks. Our strategy identifies a basket of stocks aligned with the Draghi report and the EU competitiveness agenda, which aim at closing the innovation gap, decarbonising the economy, and reducing dependencies. This framework translates into five themes: defence and security, digital autonomy, access to raw materials, energy independence and productivity, and secure healthcare and food.

- With input from Kepler Cheuvreux’s equity analysts, we have built a 15-stock equal weighted portfolio, selecting three top conviction names within each theme. Six months after launch, the strategy is delivering on expectations, up 34% as of 23 February versus 13% for the Stoxx Europe 600.

Not everything is a falling knife: bright spots in European Markets (15-stocks basket)