Before delving into Europe’s better-than-expected macro backdrop and its significance for small caps, we thought it would be relevant to share our views on the long-overdue nomination of the next Fed chair and the associated market implications.

Kevin Warsh’s nomination to be the next chairman of the Federal Reserve caused market gyrations that are worth revisiting.

- Without material insights into Warsh’s thinking, markets initially assumed his past criticism of QE and Fed dovishness in the last decade would imply a hawkish stance going forward. Last Friday, as Warsh’s nomination was unveiled, the US dollar, which had weakened markedly in the previous days, rebounded, while precious metals reversed abruptly but remain strongly up year-to-date.

- We think a sustainable rebound of the US Dollar is unlikely. First, Warsh has always been on Trump’s shortlist of candidates, and his nomination was thus priced in to some extent, though in recent weeks, Rick Rieder’s bid gained traction. Warsh’s nomination is thus unlikely to reverse recent market trends because it is not a surprise. Second, Kevin Warsh is well known for adapting his thinking to the circumstances. If Trump opted for Warsh, it is because he provided guarantees that he will push for Trump’s rate-cutting agenda in an electoral year. Third, in recent months, he aligned his view with Bessent’s, claiming that AI is a source of labour productivity gains that is disinflationary and calls for lower policy rates.

- In concrete terms, we keep hedging our USD exposures, as there is a higher probability that the EURUSD goes to 1.25 rather than reverting to 1.15, in our view.

- Warsh still has to be confirmed by the Senate, but we assume there will be no major hurdles. The key question is when the Senate banking committee hearing will take place, since two Republican senators have said that the Trump administration's threat to indict Powell could delay the confirmation process for future Fed nominees.

Turning to Europe and to the key topic addressed in our weekly report, we note that the macro backdrop is proving resilient, with real GDP growth in Q4-2025 at 0.3% (quarter-on-quarter), or 1.3% in annualized terms. While growth conditions remain subdued, Germany and Italy appear to be experiencing a resurgence (0.3% in Q4 in both countries, above consensus expectations), while Spain continues to grow at a strong pace (0.8%, also above expectations). Activity in France decelerated (0.2%), but this was expected. Looking ahead, there are still questions surrounding European growth prospects. It is not yet certain that the “tariff shock” has been fully digested. Still, overall, these figures point to the fact that macro resilience is not just a US market theme; it is also evident in Europe.

Economic resilience in Europe leads us to revisit European small caps. Small caps are more exposed to the domestic economic cycle than large caps and are thus more likely to benefit from reduced anxiety about growth conditions in Europe. Also, developments around Greenland have sharpened the focus on the need for Europe to reassert its sovereignty, a structural theme that tends to favour SMIDs given their greater exposure to local supply chains, reshoring, and domestic demand. At the same time, Greenland-related and broader geopolitical risks have supported the EUR/USD, as investors are now demanding a higher USD risk premium. A stronger euro typically favours more domestically oriented SMIDs, and we expect a higher EUR/USD by end-year.

Looking ahead, our stance on SMID caps remains constructive, although near-term upside may be constrained by the interest-rate backdrop, which remains an important driver of performance. Indeed, heightened geopolitical tensions tend to push long-term bond yields higher through an increased term premium, while the bar for an ECB rate cut in Q1 remains high, particularly given the stickiness of services inflation (see our ECB preview in the report). That said, we remain confident that the rate environment will become more supportive later in 2026 (we expect the 10-year Bund yield to decline towards 2.4% by year-end), with the window for ECB rate cuts potentially reopening later this year. ECB easing could also materialise sooner than expected should the ongoing upward repricing of the EUR/USD accelerate meaningfully, raising concerns about deflationary pressures.

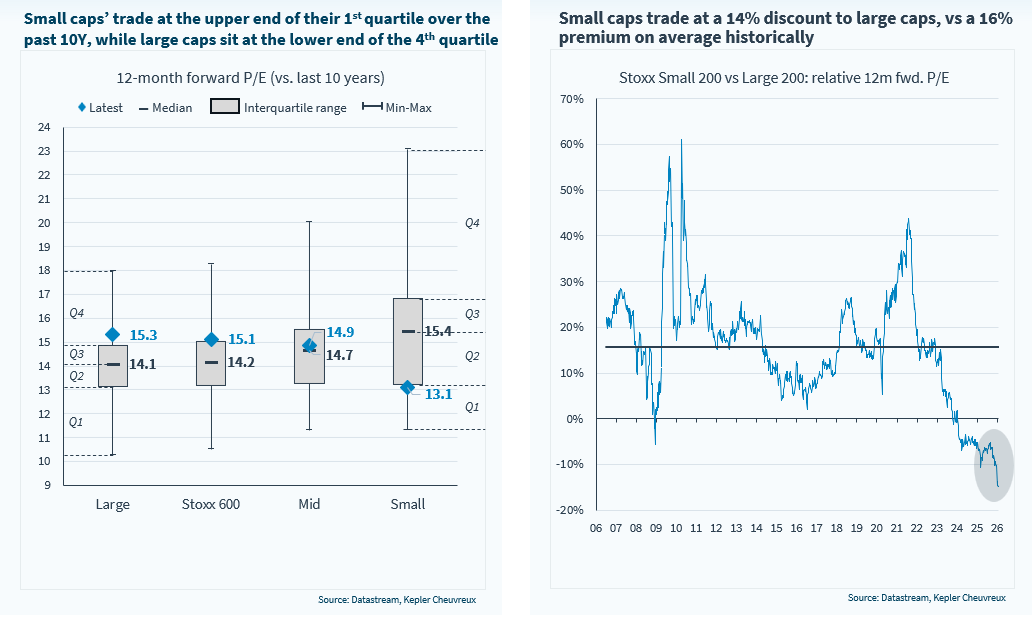

From a valuation standpoint, SMID caps continue to offer an attractive landscape. With valuations in large caps becoming increasingly demanding, relative value considerations may encourage investors to look further down the market-cap spectrum. The Stoxx Small 200 currently trades at 13.1x (materially below its 10-year median of 15.4x), while the Large 200 is at 15.3x (vs. 14.1x 10-year median).

Finally, benchmarks can be misleading, especially in the small-cap space where market inefficiencies are greater than for large caps. Less liquidity and lower analyst coverage create alpha generation opportunities that skilled managers can capture. There is a high degree of dispersion in the performance of small-cap strategies in this context, and our buy list has performed very well despite the challenges discussed above.

Investors may increasingly turn to smaller caps in search of relative value