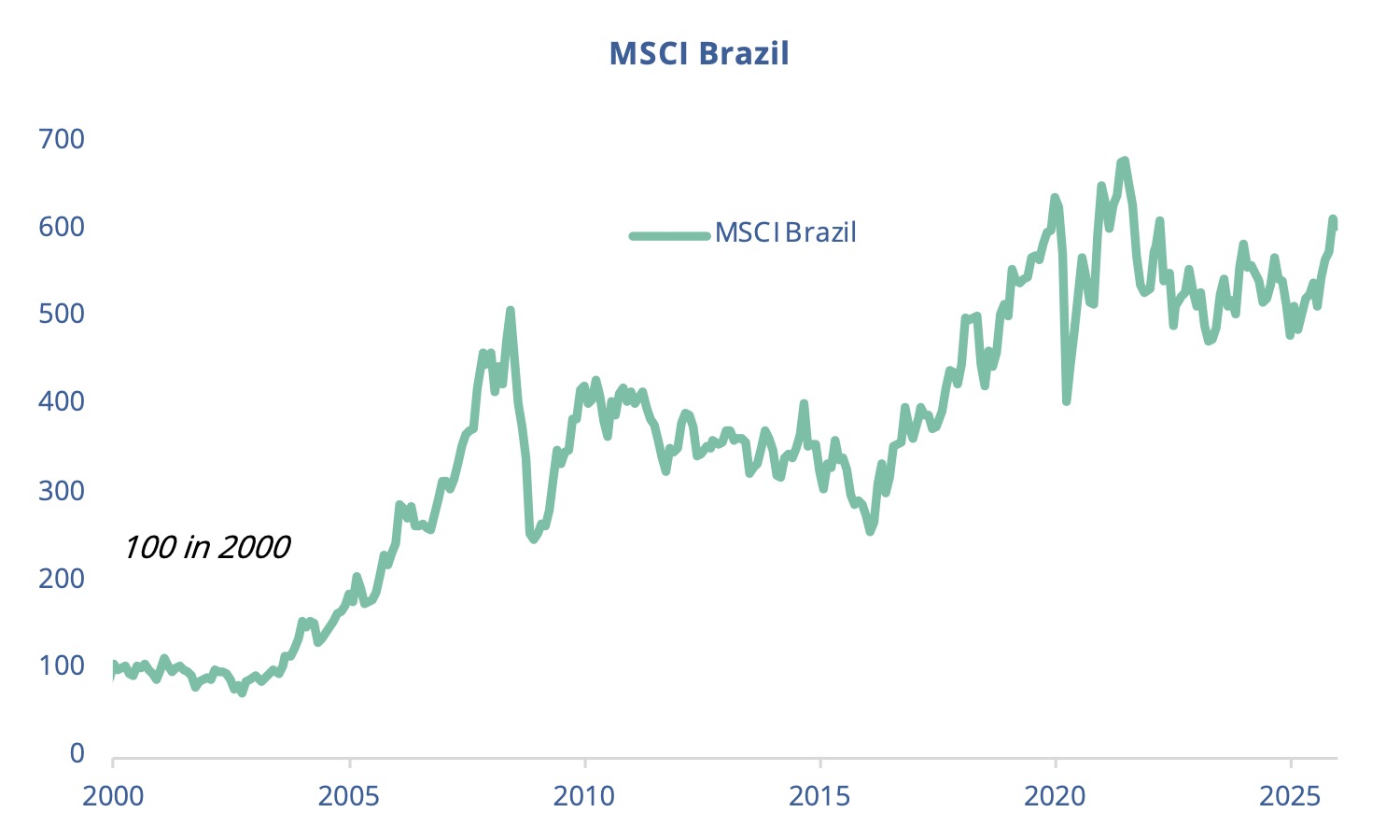

After an exceptional year in 2025 (+49.9%), Brazil remains in 2026 a key market, supported by falling rates, attractive valuations, and solid fundamentals. This analysis is part of our AMC Emerging Markets ex China product, developed in collaboration with Silex.

The recent U.S. intervention in Venezuela has put Latin America back in the geopolitical spotlight. After an already remarkable year in 2025 (MSCI Brazil: +49.9% in USD), Brazil—the region’s largest economy—should see its equity markets continue to deliver strong performance in 2026.

Starting with the international backdrop, the tariffs imposed by Washington on Brasília last August initially caused concern, but they should not have an excessively harmful economic impact on Brazil. Despite the prohibitive 50% rate floated by the Trump administration, nearly half of goods are in fact exempt and taxed at only 10% due to their strategic importance (notably aerospace and energy). In addition, the U.S. share of Brazilian exports has been steadily declining since the start of the century. It is now only slightly above 10%, far behind China at close to 30%.

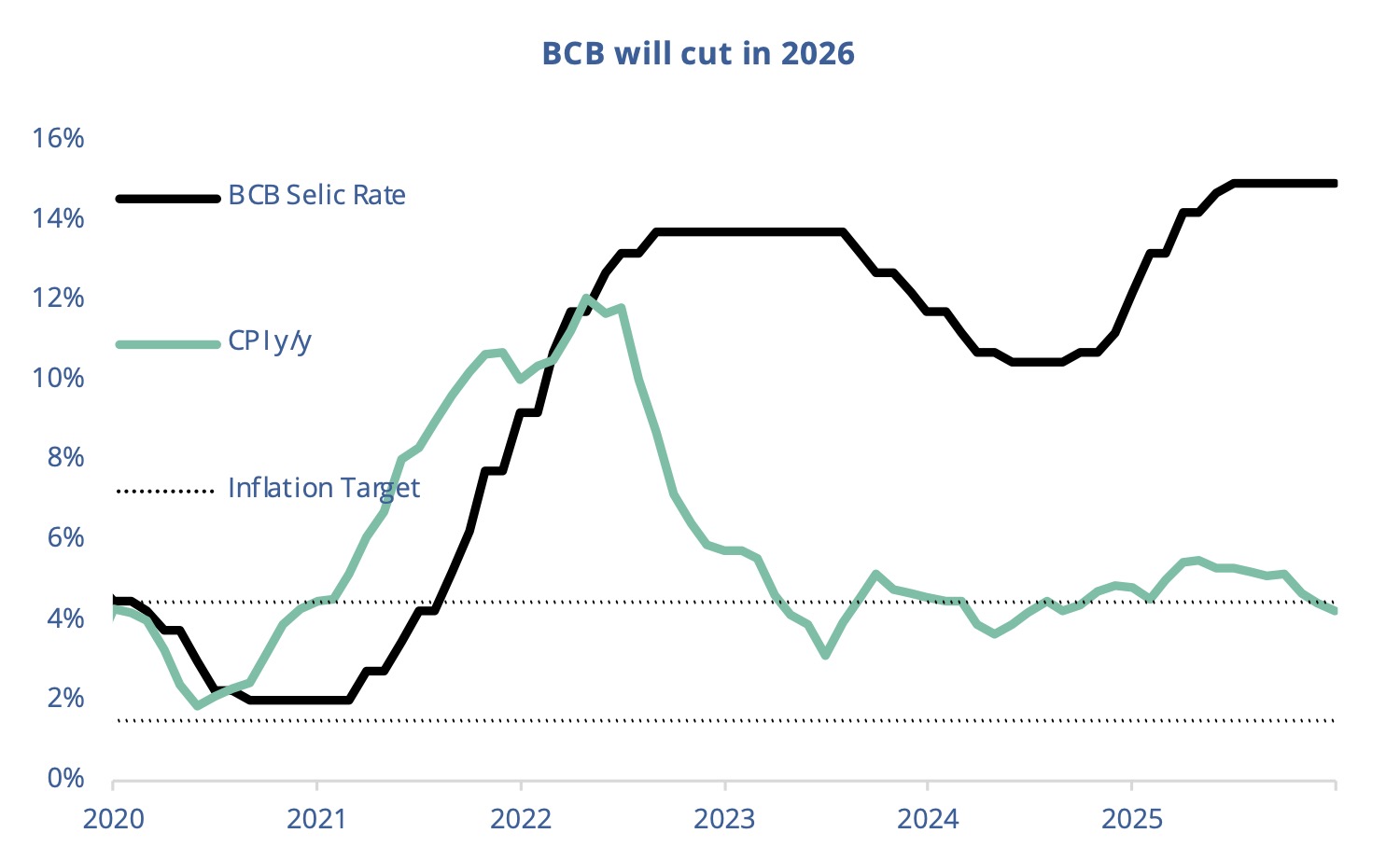

Domestically, the expected rate-cutting cycle by the BCB (Central Bank of Brazil) should provide welcome support to the economy and markets. The BCB kept its policy rate at 15% throughout the second half of last year, ultimately managing to bring inflation back under control (4.26% y/y in December, i.e., back within the 3% +/- 1.5% band targeted by the central bank). Although growth has slowed due to extremely restrictive real rates, it has held up (GDP: +1.8% y/y in Q3 2025), and early signs of a rebound are beginning to emerge: the Composite PMI moved back above 50 in December (52), returning to expansion for the first time since March.

Brazilian equities are also well positioned to benefit from a rebound in commodity prices such as iron ore (Vale) and oil (Petrobras), both of which have been trending lower for several years. This also helps explain why Brazilian stocks are very cheap, with the MSCI Brazil trading at only 9.3x next-twelve-month earnings as of December 31.

Finally, the timing may be attractive with less than a year to go before the presidential election. In December 2025, Jair Bolsonaro (sentenced to 27 years in prison) refused to back the moderate candidate from the conservative camp, Tarcísio de Freitas, instead favoring his son Flávio. On this news, markets corrected quite sharply: divisions within the opposition would effectively pave the way for a fourth term for Lula, whom investors view as a headwind for equities due to the less “pro-business” orientation of his economic policies. This unexpected shift has created an interesting entry point and offers positive optionality in case of an electoral surprise in October next year.