A wave of optimism fueled a rebound in both equities and bonds yesterday, as WTI fell toward $95/b. However, it remains to be seen whether this momentum can be sustained. For now, there are no concrete signs of conflict de-escalation in the Middle East, and crude oil futures are up 2.5-3% as we go to press. That said, the fact that some vessels have been “authorised” to cross the Strait of Hormuz in recent days, alongside Iranian crude continuing to be shipped out of the Gulf under normal conditions (mainly to China), is clearly encouraging. This effectively amounts to a partial reopening of the Strait, which could help ease market concerns by muting the transmission channel from geopolitics to financial markets.

No global escalation. The refusal that met Trump’s request for support from his “allies” to secure the Strait of Hormuz is telling. It highlights how the past twelve months of pressure and threats related to trade wars, not to mention Greenland, have contributed to isolating the US administration on the global stage. In effect, the rest of the world appears to be telling Trump to clean its own mess. The absence of broader international involvement in the conflict could ease the movement of oil tankers to Asia, the primary destination for crude oil and petroleum products transiting through the Strait. Roughly half of China’s crude oil imports (5 mb/d out of 11.6 mb/d) pass through the Strait, including an estimated 1.3–1.5 mb/d of Iranian crude currently being shipped out.

Ideas for positioning around a partial reopening. European and Asian equities have underperformed the most since the onset of the conflict, given their status as major energy importers. Europe has also seen a sharp rise in gas prices, putting upward pressure on bond yields as markets price in higher inflation and the risk of widening budget deficits should governments reintroduce energy subsidies. Rebuilding exposure to month-to-date underperformers, such as European equities, EM Asia and Japan equities, Italian BTPs in sovereign bonds, as well as banks and consumer sectors in Europe, would be the most compelling strategy, though it remains risky at this stage. Assuming a partial reopening scenario materialises, with no de-escalation in the conflict in the near term, we would be comfortable increasing exposure to EM Asia and Japan equities, Italian BTPs, and European banks.

Secular thematics for a complex world. Even if a swift resolution to the current conflict were to materialise, the Hormuz crisis will leave lasting scars. Military spending is set to rise further, reinforcing defense as a structural investment theme in our view. At the same time, initiatives around sovereignty and energy independence are likely to accelerate. In this context, we believe our sovereignty and nuclear revival strategies are well-positioned to address the challenges ahead.

- Our European sovereignty strategy is designed to align with the implementation of the Draghi report. It is structured around five key sub-themes: security and defense, energy independence, digital autonomy, access to raw materials, and secure healthcare and food systems. For each of these, we identified three high-conviction stock ideas with our equity analysts. Since its launch in mid-2025, the strategy has delivered strong outperformance versus its benchmark.

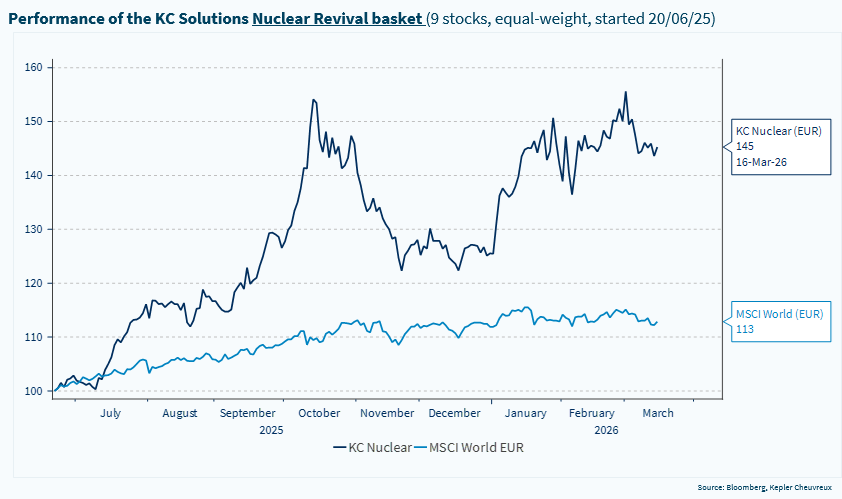

- Nuclear power is re-emerging from the current geopolitical context as a key lever to strengthen security of energy supplies. It provides a credible pathway to reduce dependence on fossil fuels. Investor interest reflects this shift: according to Kepler’s TrackInsight, assets in nuclear-themed ETFs grew by more than 60% between 2023 and 2025 and will gain further traction in current conditions. Our nuclear strategy comprises nine global stocks and has delivered solid performance since inception, as detailed in this report.

Finally, we also highlight in this report that the recent repricing in European fixed income and credit is creating attractive entry points, assuming oil prices stabilise in the $80-100/b range in the near term and inflation does not re-accelerate materially. In particular, we view the circa 100bps repricing in euro area inflation swaps as an opportunity. A sustained 20% increase in oil prices (e.g. from $70/b to $85/b) would indeed put upward pressure on inflation in the region, but likely by only around 0.5 percentage points by year-end. Our central assumption is that the current environment differs materially from 2022, when Russia–Ukraine-related disruptions compounded an already strong post-COVID inflation shock. By contrast, in 2026, inflation had been moderating ahead of the conflict, the US labour market was gradually loosening, and wage pressures were easing, partly reflecting the growing adoption of AI.

Nuclear revival: playing energy independence and Small Modular Reactors deployment