The bearish mood that started to take shape in early August was overshadowed by rising optimism regarding a ceasefire in Ukraine. Following what the US president described as highly productive talks in Moscow between his special envoy and Putin, Trump said he would meet with Putin in the coming days.

- Ukraine’s international government bond rallied on the news and pushed some segments of European equity markets higher, in particular Autos, Chemicals, and Travel & Leisure stocks, while Telecoms and Utilities lagged.

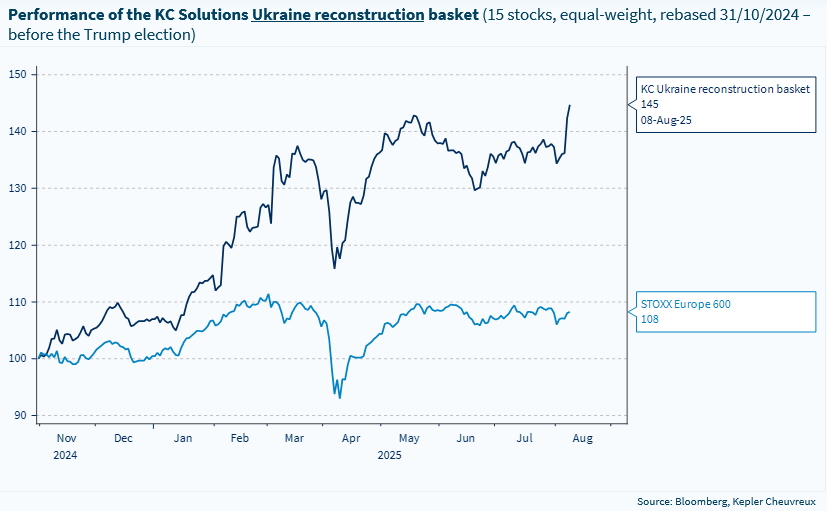

- Our Ukraine reconstruction basket of stocks is fully capturing these dynamics, with the best-performing stocks in the past few days being Raiffeisen Bank, CRH, Arcelor Mittal, BASF and Heidelberg Materials. We provide an update on the basket in the report.

As the peak summer season is here, we thought it would be appropriate to focus on the Travel & Leisure sector (OW rating). Last week, we adopted a more cautious view on European equities for the coming months. Yet, we believe that Travel & Leisure should continue to benefit from supportive top-down trends. In particular, we expect oil prices to remain weak on the back of massive oversupply conditions, which should notably continue to boost the Airlines segment (c. 40% of the index). On top of that, a potential cease-fire in Ukraine would be a major tailwind for the sector, given the negative implications for oil prices and as lower geopolitical tensions would likely provide a boost to consumer confidence in our region. Some degree of caution is warranted here, as three rounds of talks between Ukraine and Russia since May have failed to bring the war closer to an end.

Although the Travel & Leisure sector is not directly exposed to tariffs per se, the uncertainty induced by trade wars has dampened travel plans, especially for Americans. The lodging segment (c. 30% of the index) has lagged the broader sector this year, as it benefits less from falling oil prices than Airlines. Although visibility remains rather low in H2 for hoteliers, the strong appetite for travel since Covid points to a lasting shift in consumer behaviour towards valuing experiences - especially premium ones - over goods.

Week ahead: The US CPI & PPI will be the key highlight of the week, considering the market sensitivity around the impact of trade tariffs on inflation and monetary policy. In the euro area, the second estimate of the Q2 GDP will be available. In China, new loans and aggregate financing data will be released, as well as home prices, retail sales, and industrial production.

Kepler Cheuvreux’s Ukraine reconstruction basket has captured the higher probability of a ceasefire