Amid renewed geopolitical tensions at the start of 2026, gold and silver entered another leg higher. Notably, prices have continued to advance even as tensions surrounding Greenland have eased in recent days. The “America First” agenda, together with the Greenland episode, has heightened the risk of capital protectionism, contributing to a gradual de‑dollarisation of the global financial system.

- Given the lack of credible alternatives to the US dollar as a global reserve asset, precious metals are likely to remain key beneficiaries of this ongoing “aurification” trend.

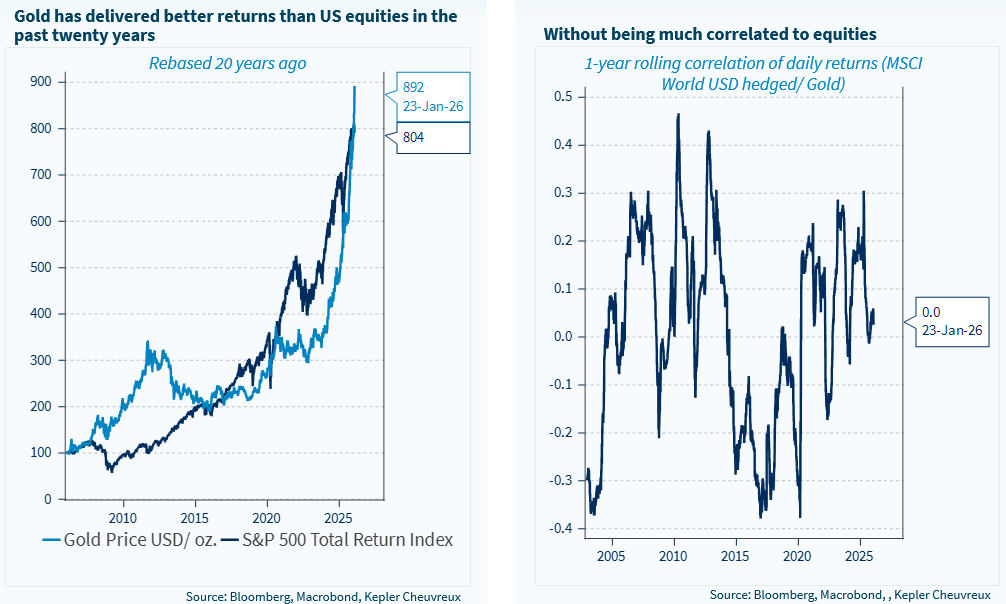

- As shown in this report, despite its exponential rise in recent quarters, gold continues to offer attractive diversification benefits. Over the past twenty years, gold has outperformed the S&P 500 in total return while exhibiting no meaningful correlation with global equities. The one‑year correlation with equities currently stands at exactly zero, based on weekly returns.

Gold ETFs have seen massive inflows over the past twelve months, potentially reflecting increased retail participation and early signs of froth. In addition, central banks are sitting on substantial unrealised capital gains and could, in theory, be tempted to sell part of their gold holdings to support public finances. The market value of US official gold holdings has surged to around USD 1.4 trillion. Nevertheless, we view widespread central bank selling as unlikely. Emerging market central banks have, in fact, continued to add to gold reserves in recent months, albeit at a slower pace than the exceptional accumulation observed in 2022.

Looking ahead, gold prices remain heavily influenced by the USD, given that gold is priced in dollars. Our outlook for the USD remains negative. Beyond President Trump’s controversial policy agenda, the upcoming nomination of the next Fed chair could also revive expectations of rate cuts, another bearish factor for the dollar. Our estimates suggest that the beta of gold versus the DXY is exactly 1, implying that a 10% decline in the dollar corresponds, on average, to a 10% rise in gold prices over the past twenty years. Last year, however, this relationship was far more extreme, with the DXY falling 10% while gold surged by 65%.

Silver and gold mining equities offer alternative, higher‑beta avenues to gain exposure to the precious‑metals theme. As detailed in this report, silver prices have risen sharply since last November, driven by persistent physical supply deficits, declining inventories, and record‑high industrial demand.

- Historically, silver has acted as a leveraged play on gold, exhibiting a twenty‑year beta of around 1.4, a sensitivity that has increased markedly in recent months.

- Gold mining equities have likewise outperformed the metal itself, consistent with their long‑term beta of approximately 1.7 to gold prices. Valuations across the gold‑mining sector remain broadly in line with historical averages; however, a material pullback in gold prices would, unsurprisingly, represent a downside risk for the space.

In our view, after such a strong rally, positioning with some downside protection appears sensible across the precious metals complex, which encompasses gold, silver and gold miners. Yet, erosion in perceived US policy reliability may prompt incremental de‑risking from sizeable Treasury exposures; a dynamic that could support gold prices in the USD 6,000-7,000/oz range over Trump’s current mandate.

Finally, in line with the above, we reiterate our US energy trade idea, expecting continued strength in equipment and services. We also reaffirm our positive stance on the EU sovereignty thematic, which has continued to outperform the European equity market.

Gold captures the geopolitical risk premium while enhancing portfolio diversification