Newly released information on the US economy suggests a recession is still a distant or unlikely threat.

But we don’t expect the good news on the economy to alter the Fed’s marginally dovish stance adopted in December as we head into the first FOMC meeting of 2024. This week will also be critical on the earnings front. Microsoft, Alphabet, Amazon, Apple, META will report earnings. Nvidia and Tesla already reported, and the latter was disappointing after the sales growth warning. In Europe, LVMH earnings gave a boost to the luxury sector, which we upgraded to Neutral back in December.

In today’s weekly, we share our first thoughts on US elections, a key theme for 2024. Donald Trump is gaining strong momentum in the polls, but the outcome of the election can dramatically change whether for legal (Trump) or health (Biden) reasons. As of today, there are no alternative candidates if Trump or Biden exit. We provide in the report a timeline of the key dates leading to the 2024 US elections, both with regards to the election itself and to Trump’s legal cases. Keep in mind that the Supreme Court will break its recess next week for an emergency hearing of the insurrection clause case. The ruling is expected in the following days/weeks.

Devising market implications related to the potential victory of Trump is obviously quite tricky. He is undoubtedly controversial, divisive, unconventional and unpredictable.

- “Controversial”: Trump talks about renewed trade tariff hikes to finance tax cuts. Could it really be a good decision for the US economy to start a new global trade war when inflation risks remain in the pipeline? There are pros and cons but surely it could lead to higher yields at the long end of the curve, just as the corporate tax breaks of 2017 did.

- “Divisive”: while you can already see European/ Canadian leaders being scared of a Trump mandate, Xi and Putin would likely welcome that development. Trump seems less obsessed about Taiwan and wants to stop the war in Ukraine. Sector wise, his proposed policies involve winners and losers.

- This would reinforce “strategic sovereignty/ autonomy” ambitions on the side of the UE, and we find Aerospace and Defense attractive to hedge against complex geopolitics that might not get simpler under Trump. Meanwhile, the net impact on European car manufacturers is likely to be positive, in particular for Stellantis. But this has been hotly debated with our analysts. Then, Pharma is a typical sell during election year on the back of the noise around cutting drug prices. But action is eventually unlikely to be adopted.

- “Unconventional”: we should be ready for the unexpected. Dovish pressures on the Fed, more tax cuts while cutting fiscal spending, deregulation, diplomatic innovations, etc. Trump is “unpredictable”. The “unpredictability” factor is mostly ignored by equity markets because Trump delivered a 71% total return of the S&P during his mandate with a huge tax boost (in the background of a global growth rebound). Biden hasn’t been bad for US markets though (+52% total return so far).

While US elections will gather a lot of attention, investors need to remember that both presidents actually share a lot of common points: they both have reflationary agendas and do not care much about US deficits. For that reason, one key question mark is rather whether treasury and currency markets will allow them to deliver on their promises (and will they have a favourable Congress too).

In summary, (1) the road to the elections will be a long and winding one and the immaculate disinflation scenario could still help Biden, (2) a steepening of the curve looks like a winning trade in both outcomes, (3) sector wise, Trump would boost Defence spending in Europe. Trump could also be a real game changer for the value perception of legacy auto makers' technologies, i.e thermal engines. Please open the document for more insights and engage with us on the topic!

Turning on to the follow-up of our investment scenario, last week confirmed what we eluded to in our previous weekly: The ECB pushed back a bit too hard on rate cuts in December and the ECB press conference last week gave the opportunity to Lagarde to leave the door open for an April cut (as we expect) and hence confirm they will be pragmatic. Good (at the margin) for European risk assets and bonds. We take the opportunity to switch our Gilts position into Italian BTPs.

Cross asset trade ideas: #1 buy Italian BTPs on the back of renewed flexibility from the ECB and Meloni’s fiscal orthodoxy. We cut Gilts considering potential pre-election tax cuts in the UK to boost Conservatives that are lagging vs. Labour in election polls. #2: Aerospace and defence stocks to play the strategic sovereignty/ autonomy of Europe in case Trump wins and more largely on the back of record military spending worldwide. #3: curve steepeners in EUR (ECB pivot) or in USD (Trump lifting the long end of the curve with a pro-growth agenda).

Week ahead: US ISM survey, job market report, FOMC meeting. In the euro area, watch the preliminary Q4 GDP as well as the January CPI. In China, watch the manufacturing and non-manufacturing PMIs. On the corporate earnings front, Microsoft, Alphabet, Amazon, Apple, META will report earnings, among others. In Europe, Novo Nordisk, Roche and Novartis will report earnings. European banks will see Santander, Deutsche bank, ING and BNPP reporting earnings.

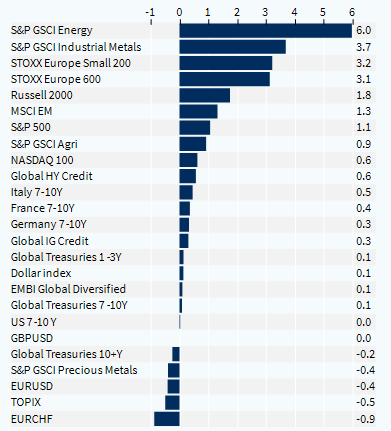

Weekly asset classes performance (%)