Risk assets retreated in the past few weeks as the probability of a worst-case scenario increased.

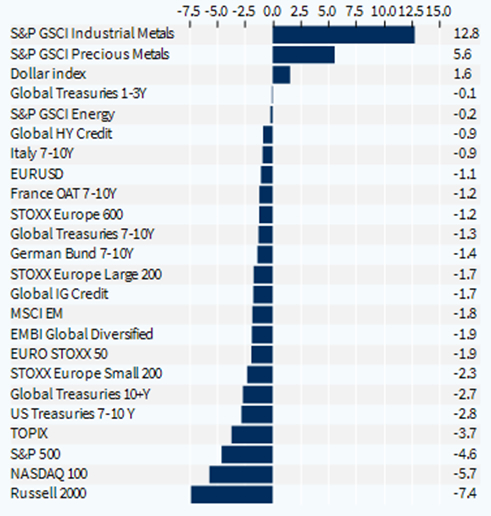

We have highlighted on several occasions that a key risk for 2024 is unstable geopolitics fuelling oil prices, and by extension inflation and rate expectations, especially in the US. In this scenario, despite their willingness to cut rates, central banks would be cornered by renewed price pressures and would have limited options than to fight inflation at any cost, putting the world economy at risk of a severe recession. The higher probability of this scenario dragged US equities down 5-6% month-to-date, as USD rates repriced 30-40 bps higher, depending on the maturity. European stocks outperformed, mainly on the back of the solid performance of the UK on which we have turned positive recently. Meanwhile, small caps underperformed both in Europe and the US on the back of their sensitivity to interest rates. Inflation hedges such as commodities outperformed, as equities and bonds went down.

Going forward, we believe geopolitical tensions have peaked, at least in the near term. None of the parties involved (US, Israel, Iran) have interest in an escalation that would cause oil prices to skyrocket and may provoke a global recession. Not even Russia might be interested in causing a major blow to the global economy as it is more dependent than ever on oil prices to finance its war economy. Energy prices would probably dramatically reverse if central banks are forced to hike further policy rates, increasing the likelihood of a recession.

The underlying macro picture remains positive as the global economy stays resilient. Some inflation caused by strong demand is actually supportive for corporate earnings growth. The earnings season that has started a few days ago keeps posting positive surprises compared to analyst expectations, both in Europe and the US. After the recent pullback, and assuming that geopolitical risks stay in check, we believe equity markets will soon revisit their late-March highs. In our model portfolio we tactically increased the exposure to the Nasdaq.

The midterm picture for risk assets is mixed. Valuations remain rich, especially in the US, and the ability of US consumers to keep spending at the current pace and support economic growth appears now more limited. Estimates of post-pandemic excess saving by the Federal Reserve signal they have now vanished. This involves headwinds for households in order to keep spending faster than revenue growth. But it does not involve either a sudden collapse in consumer spending.

Our strategic allocation remains balanced. Sources of diversification away from equities are scarce, as bonds remain under pressure and commodity prices quite elevated. The appeal of higher bond yields has, so far this year, failed to translate into positive returns. From a midterm perspective, we keep gold and EM exposure, both equities and bonds, at OW. Finally, we stay positive on the USD vs. Euro and more generally vs. European currencies although in the near-term higher risk appetite might prove supportive for the EURUSD.

Week ahead: the earnings season will kick into higher gear both in Europe and the US. Meta Platforms (Facebook), Alphabet (Google), Microsoft and Intel will report in the coming days. Amazon and Apple will report next week. On the macro front, the PCE price index, the Fed’s preferred measure of inflation, will be important to monitor later in the week.

Asset classes performance - month to date (%)