As we start 2024, everyone has recovered their senses (hopefully!) and the observations that come to mind are fourfold.

First, the resilience theme in the US remains alive. A robust labour market and excess savings accumulated during the pandemic continue to propel consumption for now, posing temporary hurdles to the year-end bond market rally. Despite relatively supportive CPI and PPI numbers for December, markets are excessively optimistic about Fed rate cuts, assuming a cumulative 160bps during the year, far more than the Fed guidance (-75 bps).

Second, the fates of equities and bonds remain closely tied. As the title of this report says, it takes two to tango. The good news we are seeing on the US economy constitutes somewhat mixed news for markets. The rise in 10Y USD swap rates seen since late December put a cap on the US equity market rally, due to its growth style bias. We slightly reduce the exposure to US equities. Yet, as the earnings season starts, large cuts to Q4 EPS estimates for S&P 500 companies reduce the risk of major disappointments. This is a battle between the micro factors (positive on EPS amid growth resilience) and the macro backdrop (higher yields dragging valuations lower).

Third, the ECB continues to bury its head in the sand, pushing euro area bond yields and the EURUSD higher. We just hope it doesn’t wait for a severe recession to materialise before signalling a pivot. It will be too late by then. Luis de Guindos, the vice-president of the ECB, was quite explicit last week: the euro area is probably already in (technical) recession. So, when Isabel Schnabel says it is too early to talk about rate cuts, we wonder when the right time might be. True, the job market remains strong in the euro area, pointing to weak labour productivity, in contrast to the US. In our view, the ECB has only pushed back on rate cuts recently in order to take a better jump forward. The ECB pushback thus puts a near-term cap on curve steepening trades.

Fourth, China remains a complex equation to solve for investors. As of mid-January, the MSCI China is down 4% year-to-date in USD terms. As our partner Macquarie notes, property was the biggest drag in 2023, and the key issue is the credit risk associated with highly leveraged developers. The ongoing property crisis is leading to a run on property developers, and the policy response so far has been to ask banks to lend them more. But the credit risks that banks are willing to take are very limited. Therefore, something to watch in 2024 is if and when the central government steps in to create a backstop. Meanwhile, CPI numbers pointed to continued deflationary pressures, which have weighed on corporate earnings. Soft earnings then led to a weak labour market, which in turn has led to a sluggish consumption recovery…

Without changing tack from our mid-term views (bullish bond duration, IG credit, curve steepeners, cautious equities, cautious cyclical equity sectors, see Eight key calls for 2024), we discuss below four ideas to hedge against further resilience in the US economy putting a floor on yields in the first months of 2024:

- Re-weight Japanese equities at the expense of US equities. Wage figures released last week comforted the BoJ, which is unlikely to move forward with rate hikes before April. As the US economy remains resilient and yields remain anchored, the Yen remains weak, a bonanza for Japanese stocks (FX hedged). But this trade will probably fade beyond Q1.

- Diversify credit exposure with US high yield to manage the duration risk embedded in investment grade credit. We are keen to increase duration in bond portfolios gradually over the course of the year. But duration trades will only fully deliver when the US economy starts to show signs of weakness.

- Stay long the US dollar vs. euro on growth weakness in the euro area. This factor has to be balanced with the current ECB pushback on rate cuts. But we stick to our view that the growth momentum differential matters more, which is bearish for the euro. With the EURUSD trading near the highs of recent months, we are comfortable with being long USD.

- Crude oil remains an inflation and geopolitical hedge. But it is far too volatile in our view and additional resources are likely to be secured by Western countries to restore security in the Red Sea. This would reduce the geopolitical premium. We continue to prefer exposure to the energy sector in European equities to outright cyclical commodities.

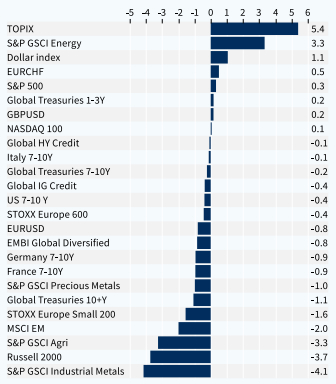

Asset classes performance (1 week)